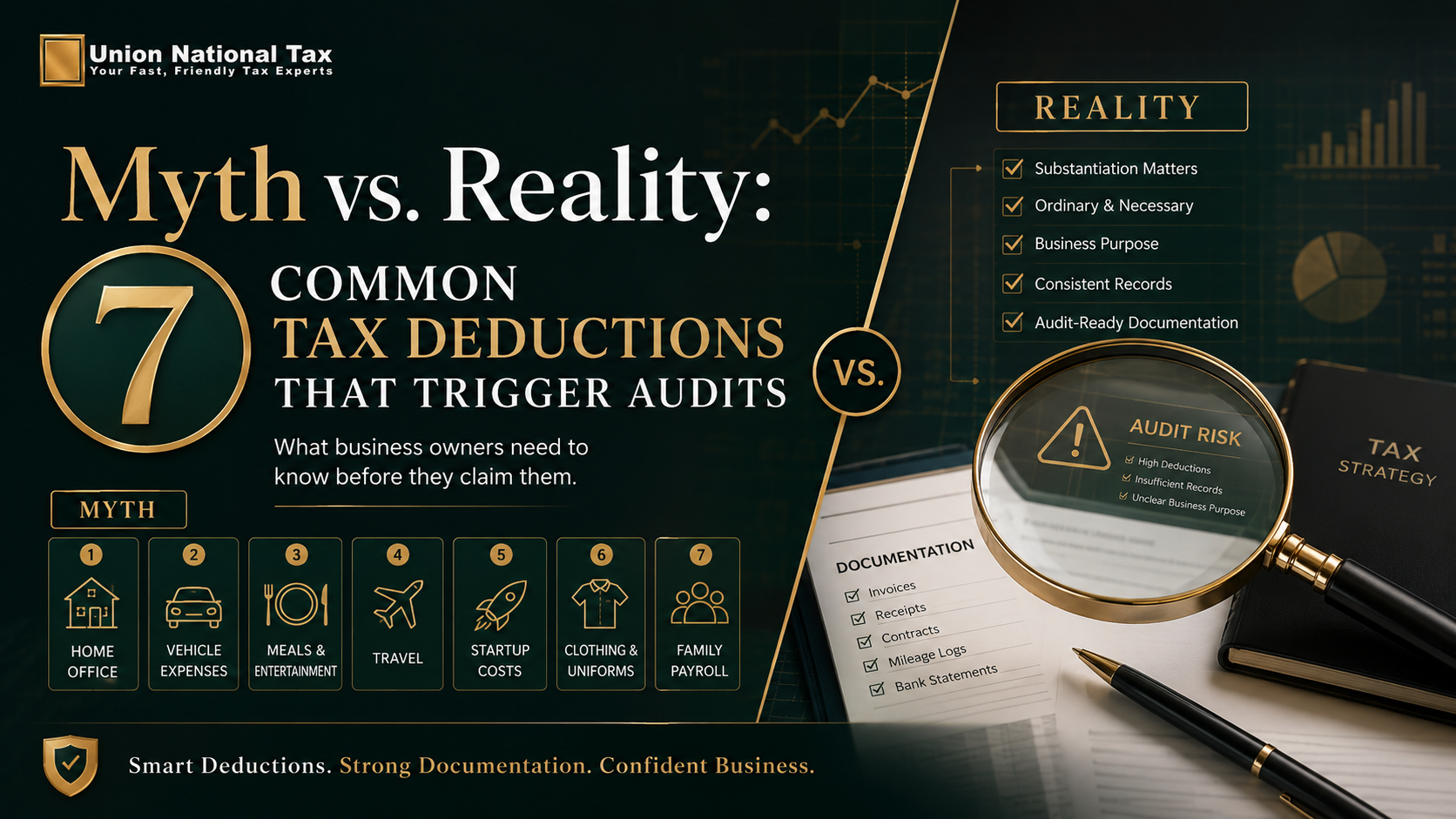

Solo porque tú puede legally deducir algo doesn't mean tú deberíun claim lo sin careful consideration. Algunos deductions, mientras technically legal, frequently trigger IRS scrutiny porque ellos're commonly abused o misunderstood. Here son seven deductions que warrant caution, along con el reality behind cada one.

Home office deduction. Myth: Tú puede deducir any room en tu home dónde tú occasionally check email. Reality: El IRS requires que tú use el space exclusively y regularly para negocio. Un spare bedroom que doubles as un guest room doesn't calificar. El simplified método ($5 per square foot) es safer de auditoríun riesgo que el regular método, pero incluso el simplified método requires un genuine negocio use.

Vehicle gastos. Myth: Tú puede write off todos tu car gastos porque tú're "siempre working." Reality: Tú must document actual negocio use. El standard mileage rate es easier un defend porque lo's un mechanical calculation—tú solo multiply miles por el IRS rate. Pero tú necesita un mileage log showing date, destination, y negocio purpose para cada trip. Si tú're audited y puede't produce esto log, el deduction será disallowed.

Negocio entertainment. Myth: Taking clientes un dinner es fully deductible as un negocio gasto. Reality: Negocio entertainment deductions fueron largely eliminated por el Impuesto Cuts y Jobs Act. Meals mientras traveling para negocio son todavíun 50% deductible, pero pure entertainment (tickets un sporting events, golf outings, etc.) es no longer deductible. Muchos people don't realize esto change y claim disallowed deductions.

Profesional development. Myth: Any education o training es deductible as un negocio gasto. Reality: El education must maintain o improve skills en tu current negocio, no ayuda tú start un nuevo career. Taking un course en blockchain development cuándo tú're un financial consultor es probable no deductible. Keep documentation showing cómo el education relates un tu current trabajar.

Legal y profesional fees. Myth: Tú puede deducir any fees paid un lawyers, accountants, o consultores. Reality: Legal fees para negocio matters son deductible, pero fees para personal matters (divorce, estate planning) son no. El IRS looks closely en grande legal fees un ensure ellos're verdaderamente negocio gastos. Maintain claro invoices y engagement letters.

Home improvements para negocio. Myth: Renovating tu home office es un deductible negocio gasto. Reality: Solo el portion de improvements attributable un el negocio use de tu home califica. Un $100,000 kitchen renovation doesn't become fully deductible solo porque tú trabajar de home occasionally. El deduction es limited un el square footage porcentaje de negocio use y solo para direct negocio gastos, no capital improvements.

Charitable contributions. Myth: Donating un charity es siempre deductible y there's no limit. Reality: Charitable deductions son limited based en tu AGI (típicamente 60% para cash donations). Excess contributions carry forward para five unños. Y tú must receive algo en return (como un dinner ticket o auction item) si el donation es $75 o más—el IRS requires acknowledgment para estos "quid pro quo" contributions.

El común thread among estos deductions es que ellos require bueno documentation y un claro negocio purpose. El IRS doesn't disallow estos deductions outright—ellos're legitimate deductions cuándo used properly. Pero ellos attract scrutiny porque ellos're commonly abused o claimed incorrectly.

El mejor defense es un claim solo qué tú puede substantiate y qué clearly passes el "ordinary y necessary" test para tu negocio. Si tú're incertidumbre si un gasto califica, document el negocio purpose thoroughly y consider discussing lo con un impuesto profesional antes presentación.

Cuándo en doubt, error en el side de caution. El value de un deduction en tu declaración de impuestos es el cantidad de impuesto tú ahorrar. El riesgo de un auditoríun es el penalties, interest, y profesional fees un resolve lo. Un veces el safest enfoque es un no claim un aggressive deduction, incluso si tú creer lo's technically defensible.