Failing to pay quarterly estimated taxes is one of the most costly mistakes self-employed professionals make. The penalties and interest from underpayment can eat into your savings and create unnecessary stress during an already complicated time. Yet understanding quarterly estimated taxes doesn't have to be overwhelming. Here's exactly how to stay compliant and avoid those painful surprises.

As a self-employed individual, you're responsible for paying taxes on your income as you earn it, not just at tax time. The IRS requires you to pay estimated taxes quarterly if you expect to owe at least $1,000 in taxes for the year. This includes both income tax and self-employment tax combined.

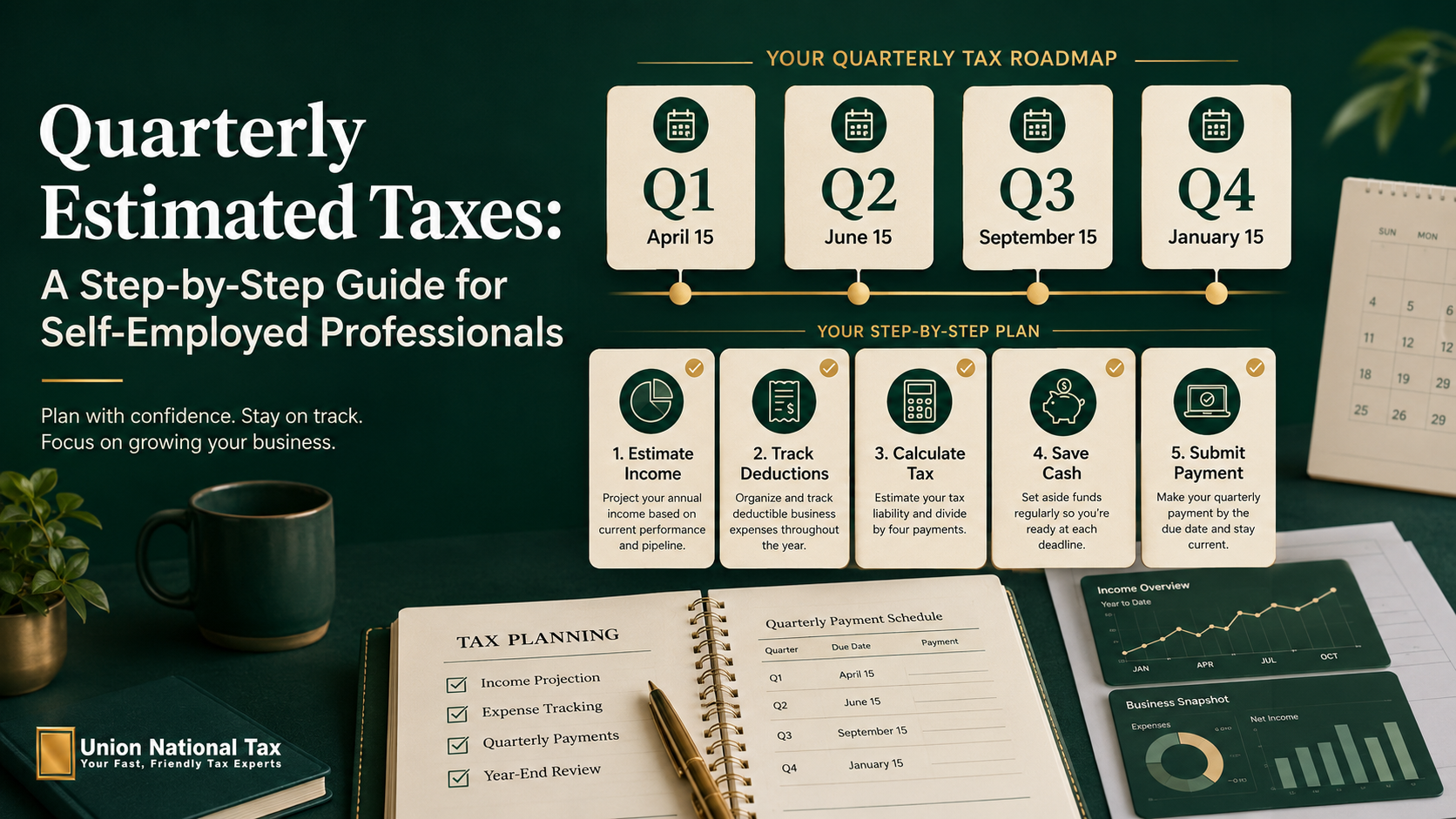

The four quarterly payment due dates are April 15, June 15, September 15, and January 15 (the following year). These dates apply to calendar-year taxpayers. If any due date falls on a weekend or holiday, the deadline shifts to the next business day.

Calculating your quarterly payment doesn't require you to be a math wizard. The simplest method is to look at last year's tax return and divide last year's total tax liability by four. This is called the "prior year safe harbor" method—it protects you from penalties as long as you pay at least 100% of last year's tax liability (110% if your AGI was over $150,000).

But if your income fluctuates significantly year to year, you might want to use the "current year" method, which estimates this year's income and calculates what you should owe. To do this, estimate your total annual income, subtract your expected deductions, and calculate the tax on that amount. Then divide by four.

Here's a practical example. Let's say you expect to earn $150,000 in net profit this year, and you estimate $30,000 in deductions, leaving you with $120,000 in taxable income. After accounting for self-employment tax and income tax combined, you might owe roughly $35,000 for the year. Dividing by four, you'd need to pay $8,750 per quarter.

You have several options for making these payments. The IRS offers the Electronic Federal Tax Payment System (EFTPS), which allows you to schedule payments in advance and receive instant confirmation. You can also pay via the IRS Direct Pay website for free, or use a credit/debit card (though this involves processing fees). If you prefer mail, you can send a check with Form 1040-ES voucher to the appropriate IRS address based on your state.

What happens if you don't pay enough? The IRS charges a penalty for underpayment, calculated based on the federal short-term interest rate (which is currently elevated). For 2024, the underpayment penalty rate is around 8% annually. That might not sound terrible, but it's completely avoidable with proper planning.

Many self-employed professionals make the mistake of waiting until tax season to pay what they owe. This often results in a shock to their cash flow and can lead to scrambling to come up with a large tax bill. By paying quarterly, you smooth out the tax burden and avoid that year-end surprise.

One key tip: Set aside a percentage of every payment you receive for taxes. Many financial advisors recommend saving 25-35% of your income for taxes, though your exact percentage depends on your bracket and situation. Creating a separate savings account and automating transfers makes this easier.

Working with a tax professional can take the guesswork out of quarterly payments, especially in your first few years of self-employment when you're still learning how much to set aside. They can help you calculate the right amount and avoid the penalties for underpayment.

The bottom line is this: Don't ignore quarterly estimated taxes. The penalties are real, the interest adds up, and the stress of an unexpected tax bill at filing time can be avoided with a little planning. Set up your system early in the year, calculate your payments accurately, and make paying these taxes a non-negotiable part of your business cash flow management.