Choosing the right business structure is one of the most important financial decisions you'll make as a business owner. Both LLCs and S-Corps offer liability protection, but they differ dramatically in how they're taxed. Understanding the nuances can mean the difference between keeping more of what you earn and overpaying the IRS.

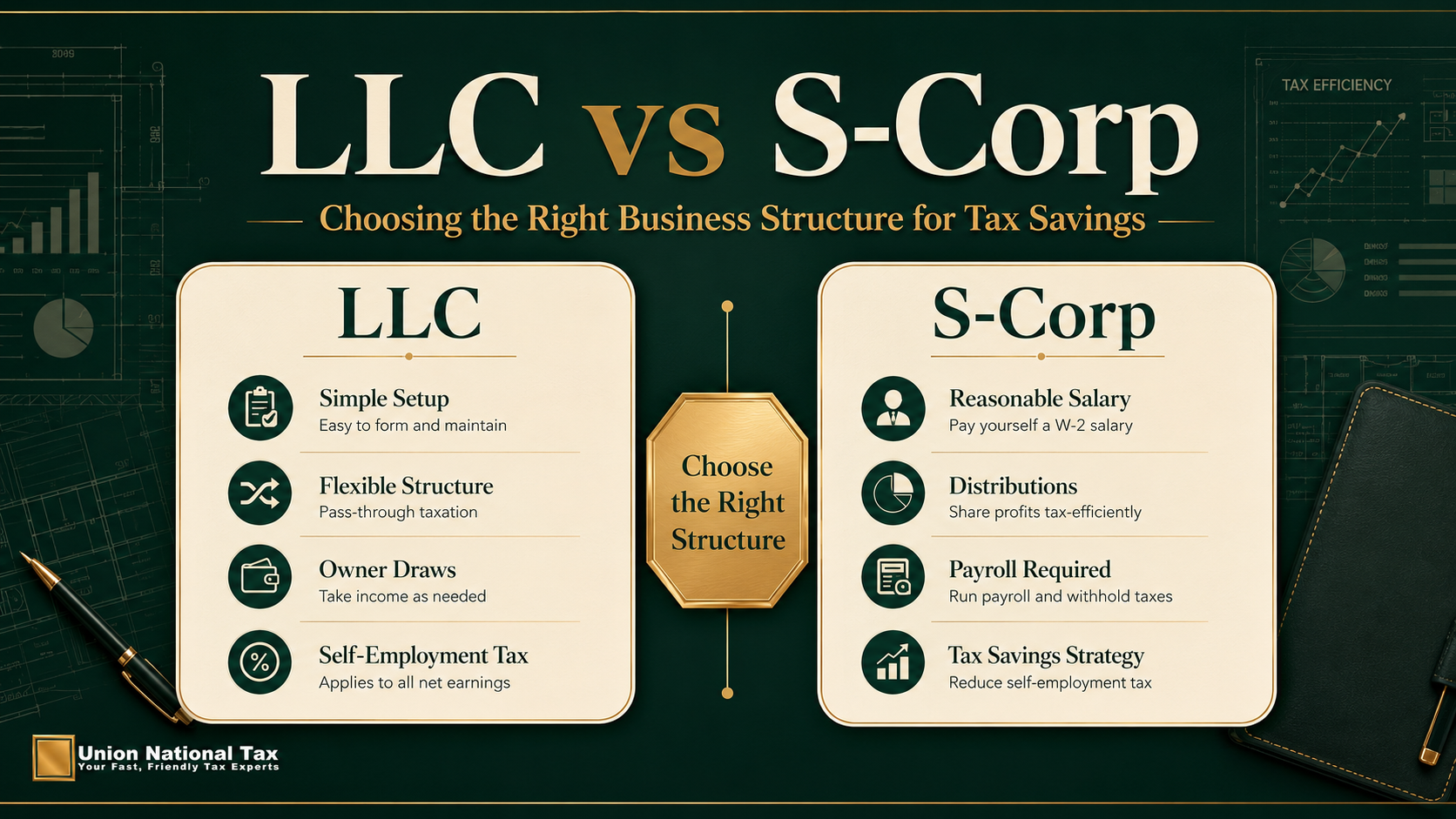

Let's start with the defaults. An LLC with a single member is taxed as a sole proprietorship by default. All profits and losses flow directly to your personal tax return, and you're subject to self-employment tax on the entire net profit. A multi-member LLC is taxed as a partnership by default, with similar pass-through taxation but with the added complexity of partnership returns.

An S-Corp election changes this dynamic. When you file Form 2553 to elect S-Corp status, your LLC (or corporation) becomes a pass-through entity for income tax purposes—but with a crucial twist. You must pay yourself a reasonable salary, which is subject to payroll taxes. Any additional profits can be taken as distributions, which are NOT subject to payroll taxes.

This is where the significant tax savings come in. Let's compare the two structures with a concrete example.

Imagine you run a consulting business with $250,000 in net profit. As a single-member LLC (sole proprietorship), you'd pay self-employment tax of 15.3% on the entire $250,000—that's $38,250. Add your income tax, and your total tax burden is substantial.

As an S-Corp, you pay yourself a reasonable salary of $100,000, which is subject to payroll taxes of $15,300. The remaining $150,000 flows to you as distributions, free from payroll taxes. You've just saved $22,950 in self-employment tax alone.

So why wouldn't everyone simply elect S-Corp status? A few reasons.

First, S-Corps require more formalities. You need to hold regular shareholder meetings, maintain corporate minutes, file separate tax returns (Form 1120-S), and run payroll—even if you're the only employee. These requirements add complexity and accounting costs.

Second, the salary requirement is real. The IRS scrutinizes S-Corp compensation closely, and setting an unreasonably low salary to minimize payroll taxes is a red flag that could trigger an audit. Your salary needs to reflect fair market value for the work you perform.

Third, S-Corps make less sense at lower income levels. The additional compliance costs might exceed the tax savings if your profit is below $80,000-$100,000. The break-even point depends on your specific situation, but as a general rule, S-Corp elections become advantageous when net profits exceed six figures.

There's also the question of flexibility. An LLC offers flexibility to choose how it's taxed—you can elect S-Corp status, C-Corp status, or remain a sole proprietorship/partnership. But once you elect S-Corp status, you're locked into that treatment for the year (and sometimes beyond, depending on IRS rules).

What about liability protection? Both LLCs and S-Corps provide liability protection for their owners. The corporate veil shields your personal assets from business debts and lawsuits, assuming you maintain proper corporate formalities. Neither structure is superior to the other in terms of protection.

The choice between LLC and S-Corp ultimately comes down to your profit level, desired lifestyle, and willingness to handle added compliance. If you're earning under $80,000 in net profit, the default LLC taxation probably makes the most sense. Above that threshold, especially above $100,000, an S-Corp election can produce significant tax savings that more than compensate for the added complexity.

Working with a qualified tax professional is essential when making this decision. They'll help you model out the tax implications of each structure and determine which approach maximizes your after-tax income. The right choice depends on your specific numbers—and those numbers change as your business grows.