The IRS audited over 1 million taxpayers last year. While audit rates are low for most individuals—less than 1% for wage earners—the risk is real, and certain red flags can significantly increase your chances of being selected. Understanding what triggers audits is the first step in protecting yourself.

First, understand how the IRS selects returns for audit. The IRS uses the Discriminant Index Function (DIF) score, which flags returns that deviate statistically from norms for similar taxpayers. The higher your score, the more likely you are to be audited. The IRS also uses document matching (comparing W-2s and 1099s to reported income) and related examinations (auditing business partners or transactions that involve your return).

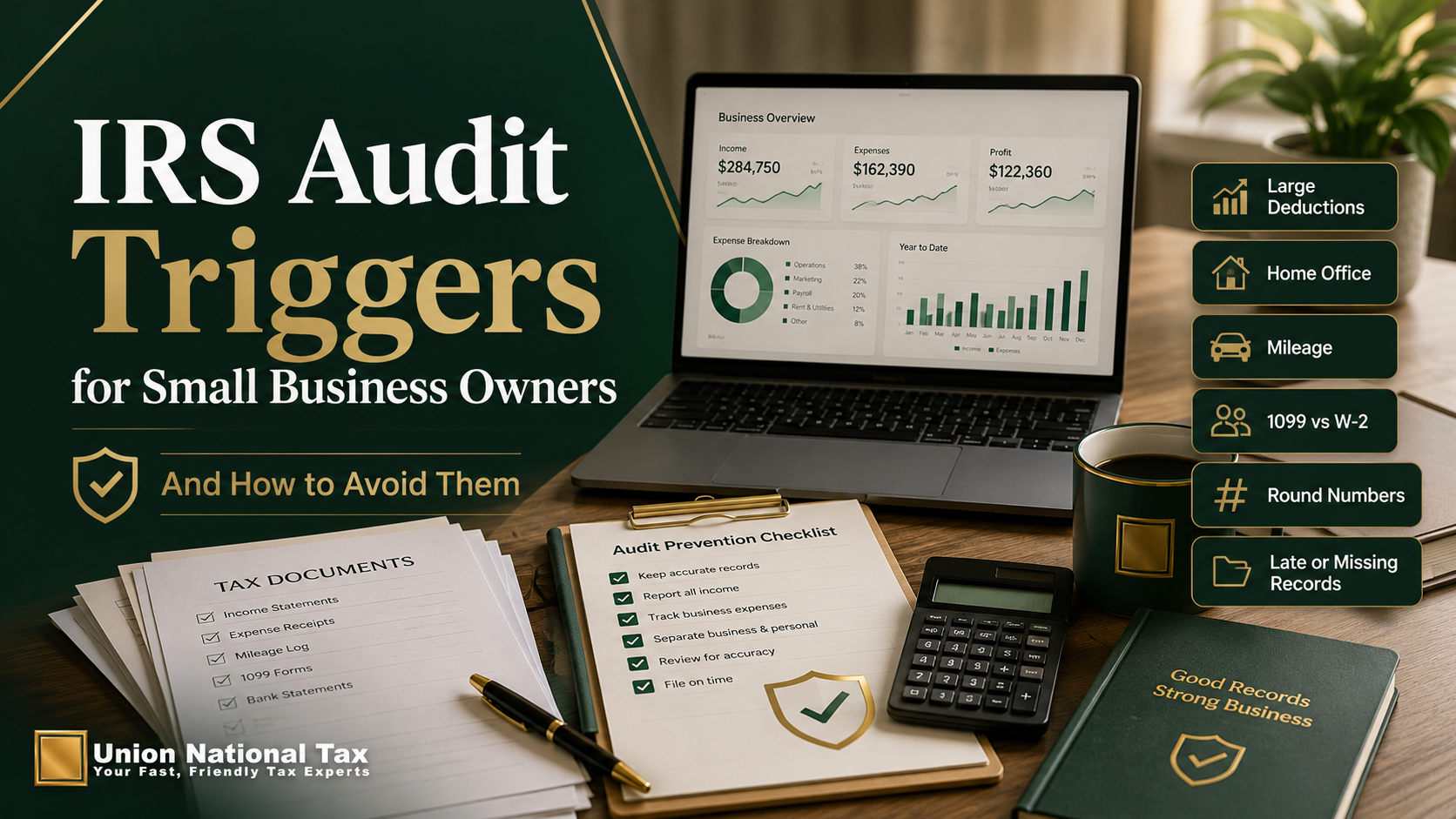

Now let's look at the specific triggers for small business owners.

High income. This is the most significant factor. Audit rates increase substantially for higher earners. For individuals earning over $200,000, audit rates begin to rise. For those over $1 million, the audit rate is significantly higher. Your business income is already scrutinized more heavily than wage income, so keeping meticulous records is essential.

Large deductions relative to income. If your Schedule C shows expenses that are unusually high compared to your revenue, the IRS will take notice. For example, if you report $200,000 in revenue but $180,000 in expenses (90% deduction rate), that looks suspicious. The IRS knows industry norms, and if you're claiming deductions well outside typical ranges, you'll likely receive scrutiny.

Home office deduction. While legitimate, this deduction is a common audit target because it's prone to abuse. Ensure you're actually using the space exclusively and regularly for business, and that your calculation method is defensible. The simplified method ($5 per square foot) is harder to challenge than the regular method, which requires calculating actual expenses.

Vehicle deductions. If you claim the standard mileage rate, the IRS knows you're likely claiming a high number of miles. Maintain a contemporaneous mileage log with dates, destinations, and business purposes. If you're claiming actual vehicle expenses, ensure the vehicle is used primarily for business—personal use of a business vehicle should be minimal.

Cash transactions. Cash businesses are particularly vulnerable to audit. If you're a restaurateur, retailer, or service provider who receives significant cash, the IRS knows you're a higher-risk taxpayer. Keep detailed records of all cash receipts and deposits.

Schedule C losses. The IRS scrutinizes businesses that report losses year after year, especially if the owner appears to have substantial income from other sources. If you're running a business at a loss, ensure you have documentation supporting the business purpose and a realistic expectation of profitability.

1099 mismatches. The IRS matches 1099 forms (from clients who paid you $600 or more) to the income you report. If you receive 1099s but underreport income, the IRS will notice. Ensure all 1099 income is reported, even if you made mistakes or didn't receive the form.

Home office expenses for employees. If you're an employee claiming home office expenses (which are no longer deductible for most employees after the Tax Cuts and Jobs Act), this is a red flag. For business owners, the home office deduction is fine, but it must be legitimate.

Charitable contributions. Large charitable donations relative to your income draw attention. If you claim $30,000 in charitable contributions on a $100,000 income, the IRS will want documentation. Keep receipts for all donations and ensure you're not claiming donations you didn't actually make.

The best defense against audits is thorough record-keeping. Keep receipts, maintain ledgers, document business purposes, and ensure everything you claim can be substantiated. If the IRS audits you and you have good records, the process is far less painful.

Consider working with a tax professional who understands audit triggers and can help you structure your return to minimize scrutiny. Proactive tax planning—rather than reactive panic—is always the better approach. The goal isn't to hide anything; it's to ensure everything is properly documented and defensible if questions arise.