How to Report Health Insurance on W-2s for S-Corp Owners

One of the most common mistakes generalist accountants make is failing to correctly report health insurance premiums for 2% (or greater) shareholders. If this isn't handled correctly on your W-2, you could lose the ability to deduct those premiums on your personal return.

The Rules for 2026

To claim the Self-Employed Health Insurance Deduction (an "above-the-line" deduction on Form 1040), the following must happen:

1. Company Paid: The S-Corp must pay the premiums directly or reimburse the shareholder (with proof of payment).

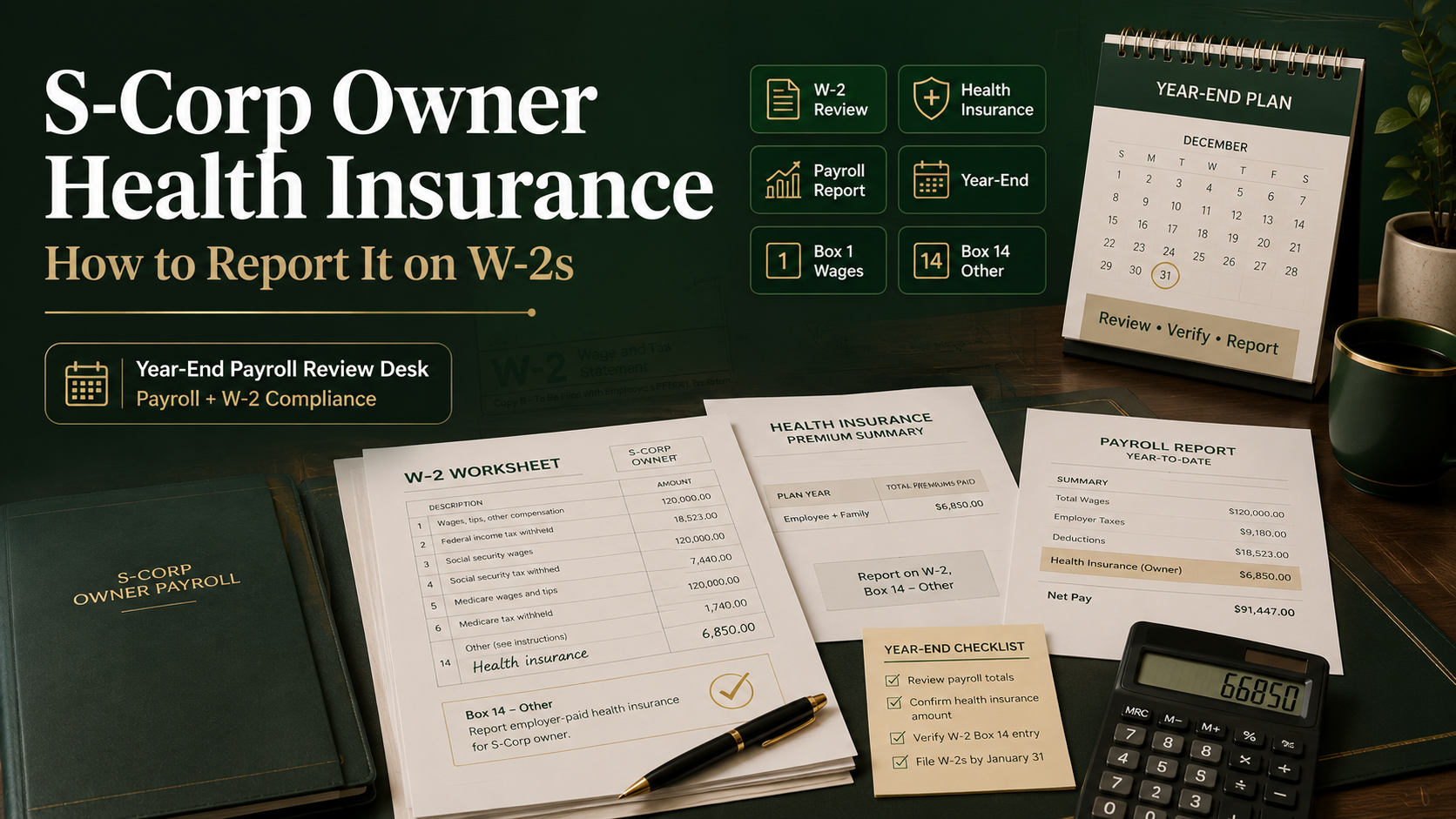

2. Reported as Wages: The amount of the premiums must be included in Box 1 (Federal Wages) on the shareholder's W-2.

3. Excluded from FICA: Generally, these premiums are not subject to Social Security or Medicare taxes if the plan is set up correctly.

The "Double Win"

When done right:

- **The Business:** Deducts the premiums as wage expense.

- **The Owner:** Deducts the premiums on their personal 1040, offsetting the income addition.

- **Result:** The benefit is effectively tax-free for income tax purposes, and exempt from FICA.

Is Your W-2 Wrong?

Check your 2025 W-2. Look at Box 14 for a code like "SCORP HEALTH." If your health insurance premiums aren't reflected there or in Box 1, your CPA might be missing a critical compliance step.

Don't leave money on the table. We review S-Corp W-2s to ensure you're maximizing every deduction available to you.