S-Corp Reasonable Compensation: The Audit Trap Most Owners Don't Know About

The S-Corp election is one of the most powerful tax strategies available to small business owners. But there's a catch that many owners—and even some accountants—get wrong.

The IRS requires that S-Corp owner-employees pay themselves a "reasonable salary." If you don't, they'll come looking—and the bill they bring is significantly worse than whatever you thought you were saving.

This guide explains exactly what reasonable compensation means, how the IRS evaluates it, and what to do to protect yourself.

What Is Reasonable Compensation — And Why Does It Exist?

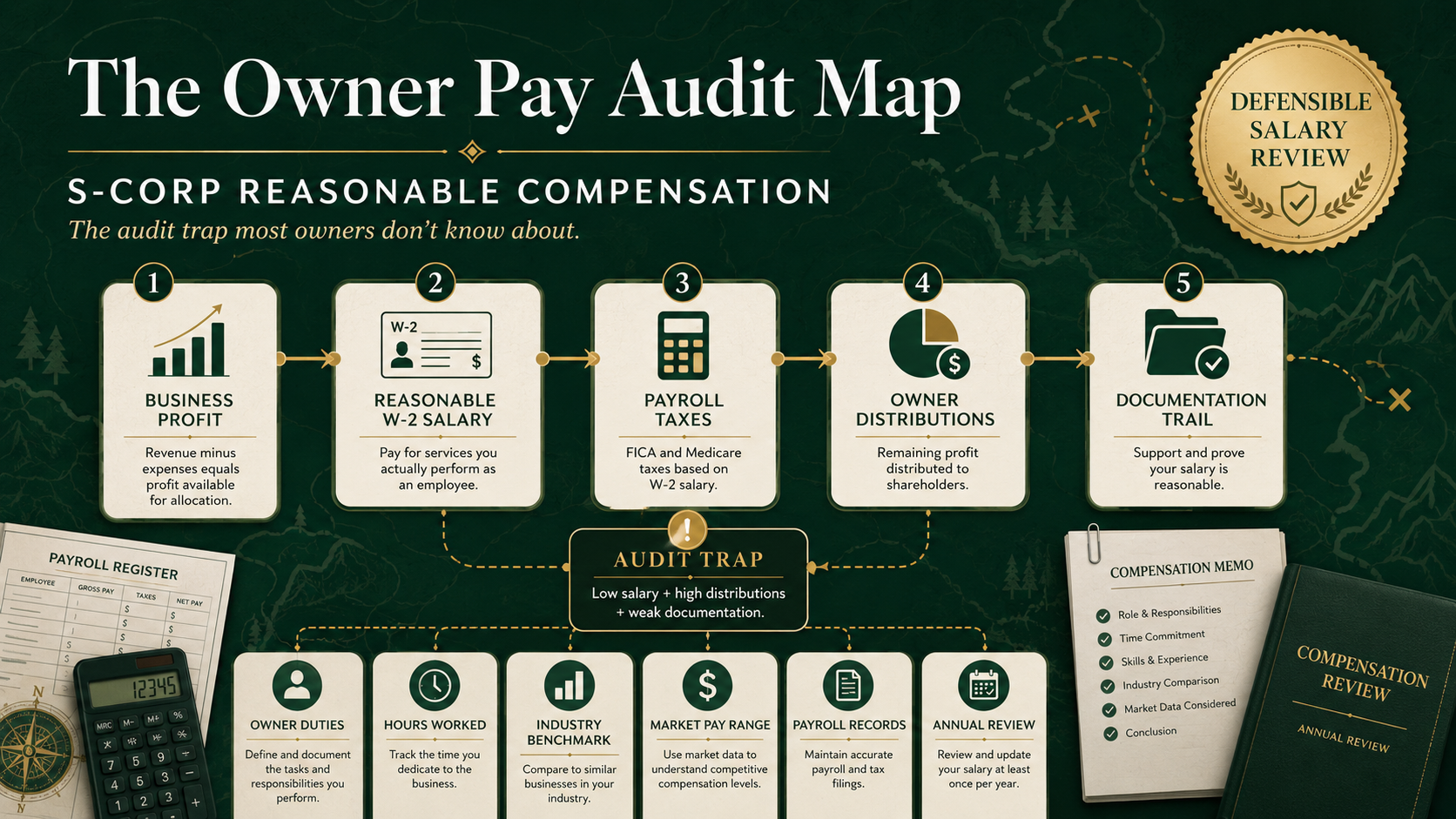

When you elect S-Corp status, your business income splits into two categories:

W-2 salary — subject to payroll taxes (15.3% SE tax split between employer and employee)

Distributions — not subject to payroll taxes

The savings come from taking more of your income as distributions. But the IRS saw that coming.

The reasonable compensation requirement exists specifically to prevent owners from paying themselves a $1 salary and taking everything as distributions to eliminate payroll tax. The law requires that your W-2 salary reflect what a reasonable, arm's-length employer would pay someone to perform your same role in the same market.

"💡 Example: If you own a $2M HVAC company and personally manage operations, run service calls, and handle sales — your reasonable compensation is very different from an owner who only handles board-level decisions and hired a GM to run day-to-day operations."

How the IRS Evaluates Reasonable Compensation

There's no single number the IRS looks for. They use a multi-factor test, which includes:

Duties and responsibilities — What do you actually do in the business?

Time and effort expended — How many hours per week?

Skill, training, and experience — What would it cost to hire someone with your qualifications?

Market comparables — What does the industry pay for your role?

Complexity of the work — Highly specialized work justifies higher compensation

Ratio of salary to distributions — A $30K salary with $270K in distributions on a $300K profit is a red flag, regardless of market data

The IRS also cross-references Form 1125-E (Compensation of Officers), which is required for S-Corps with more than $500K in gross receipts. Your numbers are visible—and they're compared against industry norms.

The Most Common Audit Trigger: The Low-Salary Approach

Some tax advisors still recommend paying yourself the smallest defensible salary to maximize distribution income. This works—until it doesn't.

Red flags that trigger IRS scrutiny:

Salary is less than 30–35% of total S-Corp net income

Your salary is dramatically below market for your industry and role

You changed your compensation significantly in the year before a tax return was filed

Your salary stays flat while distributions grow substantially year over year

"⚠️ IRS Revenue Ruling 74-44 established that if an owner-employee performs substantial services for the corporation, compensation must be paid — and it must be reasonable. This ruling is still cited in audits today."

What Happens If the IRS Reclassifies Your Distributions

If the IRS determines your compensation was unreasonably low, they reclassify a portion of your distributions as wages. The consequences stack quickly:

1. Back payroll taxes Both the employer and employee portions of FICA are assessed on the reclassified amount—that's 15.3% on the reclassified wages.

2. Interest Accrues from the original due date on each quarter's underpayment—typically going back 3 years, sometimes more.

3. Accuracy-related penalties 20% of the underpayment on top of the taxes and interest.

4. Failure-to-deposit penalties If payroll taxes weren't deposited on time, an additional 2–15% penalty applies.

"🔴 Real-world example: An owner who took $200K in distributions annually for three years with a $40K salary — and whose reasonable compensation was later determined to be $100K — could face $90,000+ in back taxes, penalties, and interest across those three years."

How to Set Defensible Reasonable Compensation

Step 1: Document Your Role

Write out what you actually do—your responsibilities, hours per week, and technical skills required. This becomes your documentation if you're ever audited.

Step 2: Research Market Comparables

Use BLS data, industry salary surveys, or platforms like Salary.com and Glassdoor to identify what the market pays for your role. Document this research and save it with your tax records.

Step 3: Apply a Defensible Benchmark

A salary that represents at least 30–40% of total S-Corp net income (profit + salary) is generally defensible. In technical fields with high market compensation, it should be higher.

Step 4: Be Consistent Year Over Year

Consistency across multiple years is itself evidence of a good-faith approach. Don't dramatically lower your salary in a high-income year to capture more distributions.

Step 5: Work with a Tax Professional Who Knows S-Corps

Not every CPA understands S-Corp compensation nuances. You want someone who has seen audit patterns in this area and can help you document your compensation methodology in writing.

Reasonable Compensation by Industry: General Benchmarks

These are starting points—your specific role, hours, and market determine the final number.

Industry

Typical Owner Role

Reasonable Compensation Range

HVAC / Trades

Active operator

$65,000–$110,000

Restaurant / QSR

Owner-operator

$55,000–$90,000

Consulting / Freelance

Solo practitioner

$80,000–$150,000

Accounting / Legal

Active professional

$100,000–$180,000

Construction (GC)

Project management + operations

$75,000–$130,000

Reasonable Compensation Checklist

Before filing your S-Corp return, confirm the following:

Your W-2 salary is documented and reflects market rate for your role

You've kept records of your duties, hours, and responsibilities for the year

You've reviewed comparable salaries in your industry and saved the documentation

Your salary is at least 30–40% of total S-Corp net income

Your payroll tax deposits were made on time throughout the year

Form 1125-E is accurately completed if your gross receipts exceed $500K.

Your compensation strategy has been consistent across the past 2–3 years

FAQ — S-Corp Reasonable Compensation

What is the IRS's definition of reasonable compensation? The IRS defines it as the amount that would ordinarily be paid for like services by like enterprises under like circumstances. In practice, it means the market rate for your role, your industry, and your market.

Is there a safe harbor salary percentage? Not officially—but a salary representing at least 30–40% of total net income (profit + salary) is widely considered defensible. Technical professionals with high market rates should lean higher.

Can I change my salary each year? Yes, but dramatic reductions in high-income years are a red flag. Consistency and documentation matter.

What if I can't afford to pay myself a market salary? If the business can't support a reasonable salary, that's a legitimate factor the IRS considers. Document the financial constraints clearly—with P&Ls—in case you're audited.

Do I need a formal compensation study? Not required, but recommended every 2–3 years for high-income S-Corps. A written compensation analysis prepared by a tax professional provides strong audit protection.

Don't Let a Good Strategy Become an Expensive Mistake

S-Corp election is still one of the best tax tools available. The reasonable compensation requirement is manageable — if you understand the rules and set your salary correctly from the start.

The cost of getting a compensation analysis done proactively? A few hundred dollars. The cost of an IRS reclassification after three years of underpaying yourself? Tens of thousands.

Union National Tax helps S-Corp owners set defensible compensation, document it correctly, and stay compliant without leaving savings on the table.