Every tax strategy conversation starts with entity selection. Most small business owners default to LLC because it's the default in most states — but default is not the same as optimal. The right entity structure can save you tens of thousands of dollars in self-employment tax. The wrong one can cost you significantly.

This is a decision that deserves real analysis, not just "what everyone does." Here's a clear breakdown.

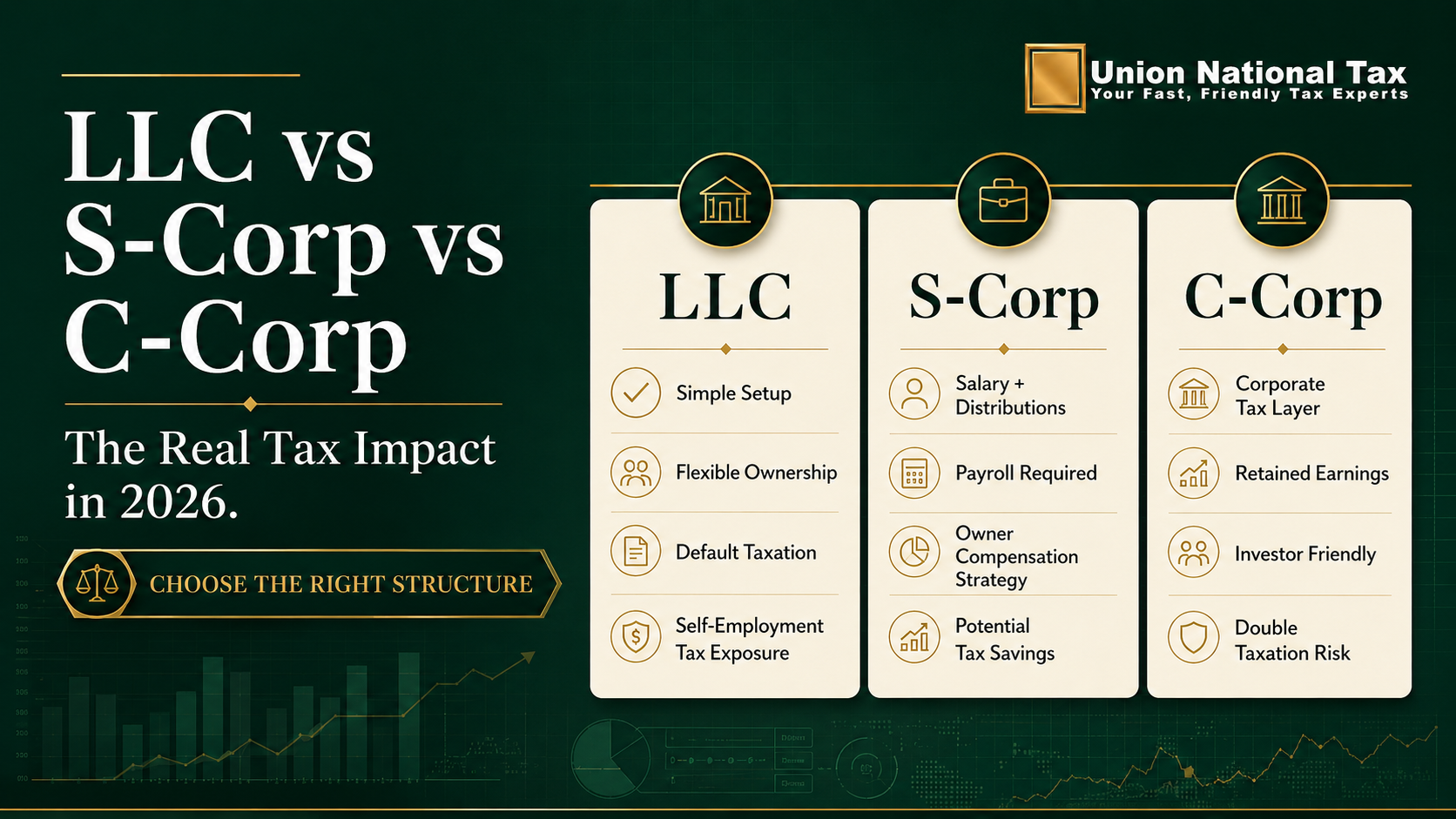

The LLC: Simple, Flexible, But Not Tax-Optimized

A single-member LLC is taxed as a sole proprietorship by default. That means all profits flow through to your personal tax return, and you pay self-employment tax (15.3%) on the entire amount. No分离 between salary and distributions. No payroll tax savings.

Multi-member LLCs are taxed as partnerships — same issue. Profits are subject to self-employment tax.

The LLC's real advantage is liability protection and simplicity, not tax savings. If your business earns under $80,000-$100,000 in net profit, the entity structure matters less. Above that threshold, an LLC alone is leaving money on the table.

The S-Corp: The Most Commonly Overlooked Tax Savings Tool

An S-Corp lets you split profits into two categories: a reasonable salary (subject to payroll tax) and distributions (not subject to payroll tax). The salary portion is taxed as W-2 income. The distribution portion is not.

This is the key distinction. In an LLC, every dollar of profit is subject to 15.3% self-employment tax. In an S-Corp, only the salary portion is.

Example: Your business makes $180,000 net profit. With a single-member LLC, you pay self-employment tax on all $180,000 = ~$27,540 in additional tax.

If you elect S-Corp status and pay yourself a $70,000 salary and take $110,000 in distributions, you pay payroll tax on $70,000 only = ~$10,710. You save approximately $16,830 in self-employment tax.

The catch: The IRS requires your salary to be "reasonable compensation" for the work you perform. They scrutinize this. If your salary is suspiciously low relative to profits, they will reclassify distributions as salary and assess back payroll taxes + penalties.

The C-Corp: Only Makes Sense at High Revenue

A C-Corp pays corporate tax (21% flat rate) on profits, then you pay personal income tax again on distributions as dividends. This is double taxation, and it's generally inefficient for businesses making under $250,000-$300,000 in net profit.

C-Corps make sense for businesses that need to retain significant earnings for reinvestment, plan to raise venture capital, or have owners in the highest income tax brackets who can benefit from the corporate rate differential.

For most growing small businesses, S-Corp is the clear winner from a tax perspective — provided the compensation is defensible.

What Determines the Right Entity for You

The decision hinges on three factors: your net profit level, your risk tolerance for audit exposure, and your state tax environment.

Rule of thumb: Under $80K net profit — LLC default is fine. $80K-$250K — strongly consider S-Corp election. Over $250K — run the numbers on both S-Corp and C-Corp. Your tax professional should be modeling these scenarios annually.

One more thing: Entity election isn't permanent. You can change structures. If you started as an LLC and you're now profitable, it's worth an annual review with your tax strategist to see if an S-Corp election makes sense going forward.

The best time to make the S-Corp election is January 1 of the tax year — or within 75 days of year-end for the current year. If you're reading this in Q4 and you expect to hit the $80K threshold this year, talk to your tax pro now about making the election.