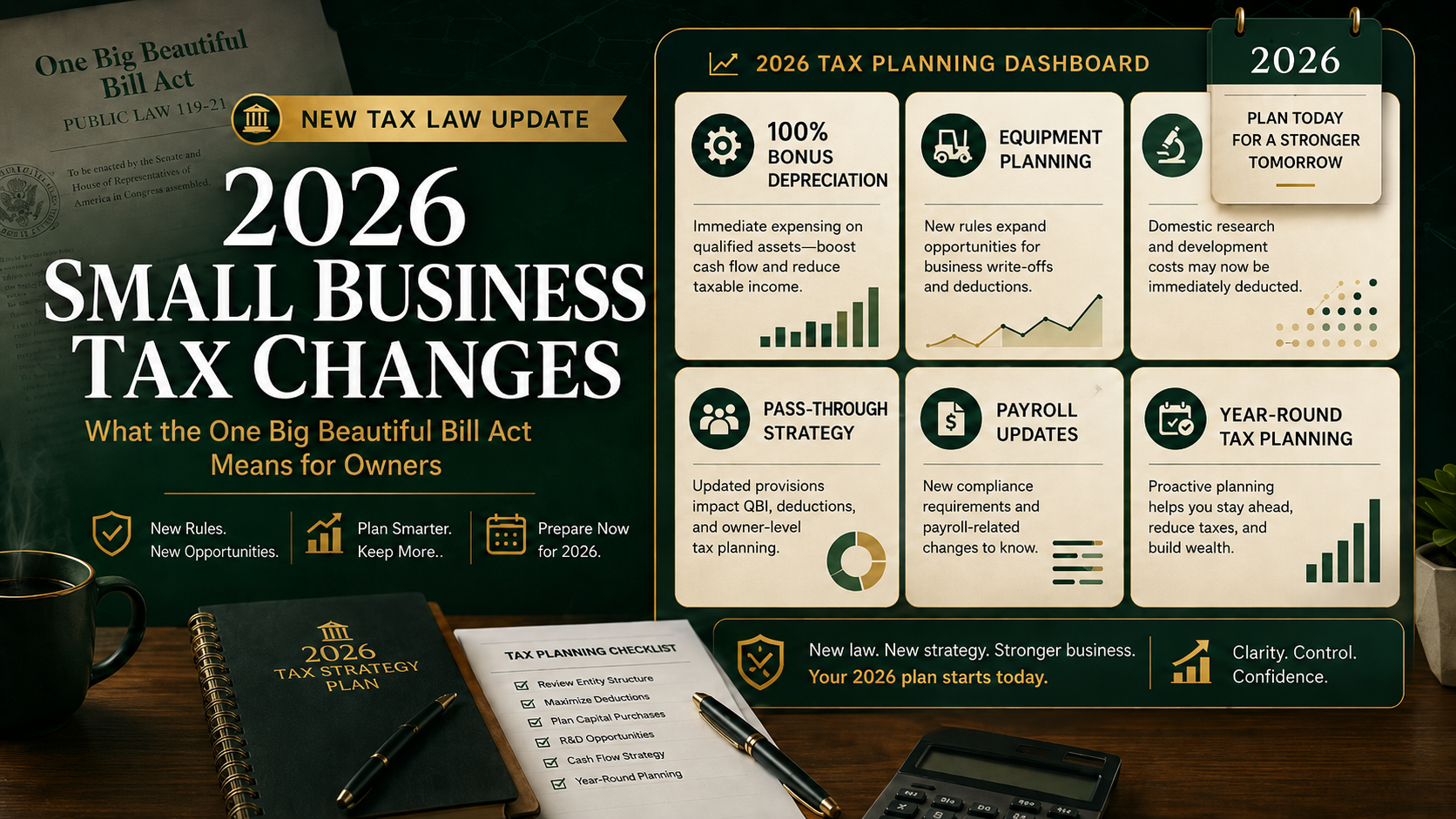

How the One Big Beautiful Bill Act Changes Small Business Taxes in 2026

The One Big Beautiful Bill Act (OBBBA) reshapes small business taxes in 2026 by locking in key breaks and tweaking how deductions, expensing, and credits work for owners. If you run a sole proprietorship, LLC, S‑corp, or partnership, it changes how much of your income is taxed, when you can write off major purchases, and which tax credits are worth planning around.

This guide breaks down the biggest OBBBA changes for 2026—tax brackets and the standard deduction, the QBI deduction, bonus depreciation and expensing, and key deductions and credits—so you can adjust your strategy before year‑end instead of reacting at filing time.

1. Tax brackets and standard deduction in 2026

OBBBA keeps the seven‑bracket individual structure (10% through 37%) but updates the thresholds and increases the standard deduction starting in 2026. That matters because most small business owners ultimately pay tax on business profit through their personal returns.

For 2026, you’ll see:

- A higher standard deduction (roughly mid‑$16k for single filers and low‑$32k for married filing jointly, with head of household in the mid‑$24k range).

- Bracket thresholds pushed up by inflation, so a bit more income is taxed at lower rates.

If you don’t have large personal itemized deductions, the larger standard deduction can reduce your taxable income and simplify your return, while you still separately deduct ordinary and necessary business expenses on your schedules.

2. QBI deduction: permanent and more planning‑friendly

The Qualified Business Income (QBI) deduction—up to 20% of qualified pass‑through income—was originally scheduled to sunset but is made permanent and adjusted under OBBBA starting in 2026.

What’s changing for small businesses:

- The QBI deduction becomes a permanent feature for eligible pass‑through businesses.

- Income thresholds and phase‑out ranges increase, giving more room before limitations fully phase out the deduction, especially for higher‑earning service businesses.

- A new, inflation‑adjusted minimum QBI deduction (starting at a few hundred dollars for businesses with at least around $1,000 of QBI) helps smaller operators receive some benefit if they materially participate.

This makes entity choice (sole prop vs. S‑corp vs. partnership) and clean bookkeeping more important, because optimizing QBI requires accurate net income and clarity on whether your work is considered a specified service trade or business.

3. Bonus depreciation and expensing: more immediate write‑offs

One of the most business‑friendly pieces of OBBBA is how it treats bonus depreciation and expensing in 2026. Instead of letting bonus depreciation phase down to lower percentages, the law restores 100% bonus depreciation for qualifying property.

For 2026 and beyond:

- 100% bonus depreciation is restored for qualifying property placed in service, so you can deduct the full cost in the year you put the asset to work.

- Used property can qualify, not just brand‑new equipment, which helps smaller businesses buying pre‑owned machinery or vehicles.

- Section 179 expensing limits and phase‑outs are increased and indexed, allowing many small businesses to fully expense equipment purchases up to higher ceilings.

Practically, this means you can front‑load deductions for equipment, vehicles, and technology, improving cash flow and cutting your current‑year tax bill—especially when coordinated with the QBI deduction.

4. Deductions and credits reshuffled

OBBBA also rebalances several deductions and credits that indirectly affect small businesses. A few highlights:

- Some clean‑energy incentives change or phase, while certain business‑energy provisions continue, so timing big energy or building projects matters.

- SALT (state and local tax) deduction rules are loosened compared with prior caps, which can help owners in high‑tax states who itemize.

- Certain business incentives—such as more favorable treatment for domestic R&D expenses—are restored or improved, allowing more costs to be deducted immediately instead of amortized over several years.

Overall, OBBBA leans toward allowing more upfront deductions and a slightly smoother landscape around some credits, but with enough complexity that you’ll want an intentional plan rather than guessing.

5. Practical planning moves for 2026

To actually benefit from these changes, build them into your 2026 plan instead of discovering them at tax time. Consider:

- Reviewing your entity structure with the QBI deduction in mind, especially if your income is near the new phase‑out thresholds.

- Mapping equipment, vehicle, and technology purchases around 100% bonus depreciation and Section 179 so you maximize deductions in the right year.

- Updating your estimated tax payments and cash‑flow projections based on your new effective rate.

- Tightening your bookkeeping so your financials clearly support QBI calculations, expensing decisions, and any credits you plan to claim.

For many owners, 2026 is a smart year for a full tax and entity “checkup” anchored around these OBBBA changes.

When it makes sense to get help

OBBBA is a long, technical piece of legislation that blends permanent changes, extensions, and new rules into one package. A proactive advisor can help you:

- Model your 2026 tax bill under different entity choices.

- Design an asset‑purchase and depreciation strategy that balances upfront write‑offs with future‑year planning.

- Make sure you’re capturing the QBI deduction and any restored or expanded credits correctly.

If you’re planning big investments, a change in how you pay yourself, or a possible entity change in 2026, getting a personalized review now is often worth far more than the cost of the advice.