If you are a profitable sole proprietor or single‑member LLC, 2026 is the year to re‑check whether your current setup still makes tax sense. With the One Big Beautiful Bill Act making the QBI deduction permanent and expensing rules more generous, an S‑corp election can cut self‑employment taxes—but only if your numbers and salary strategy truly support it.

This guide walks through when a move from sole prop to S‑corp is worth exploring, how the 2026 rules shape that decision, and what to watch so you do not swap one set of headaches for another.

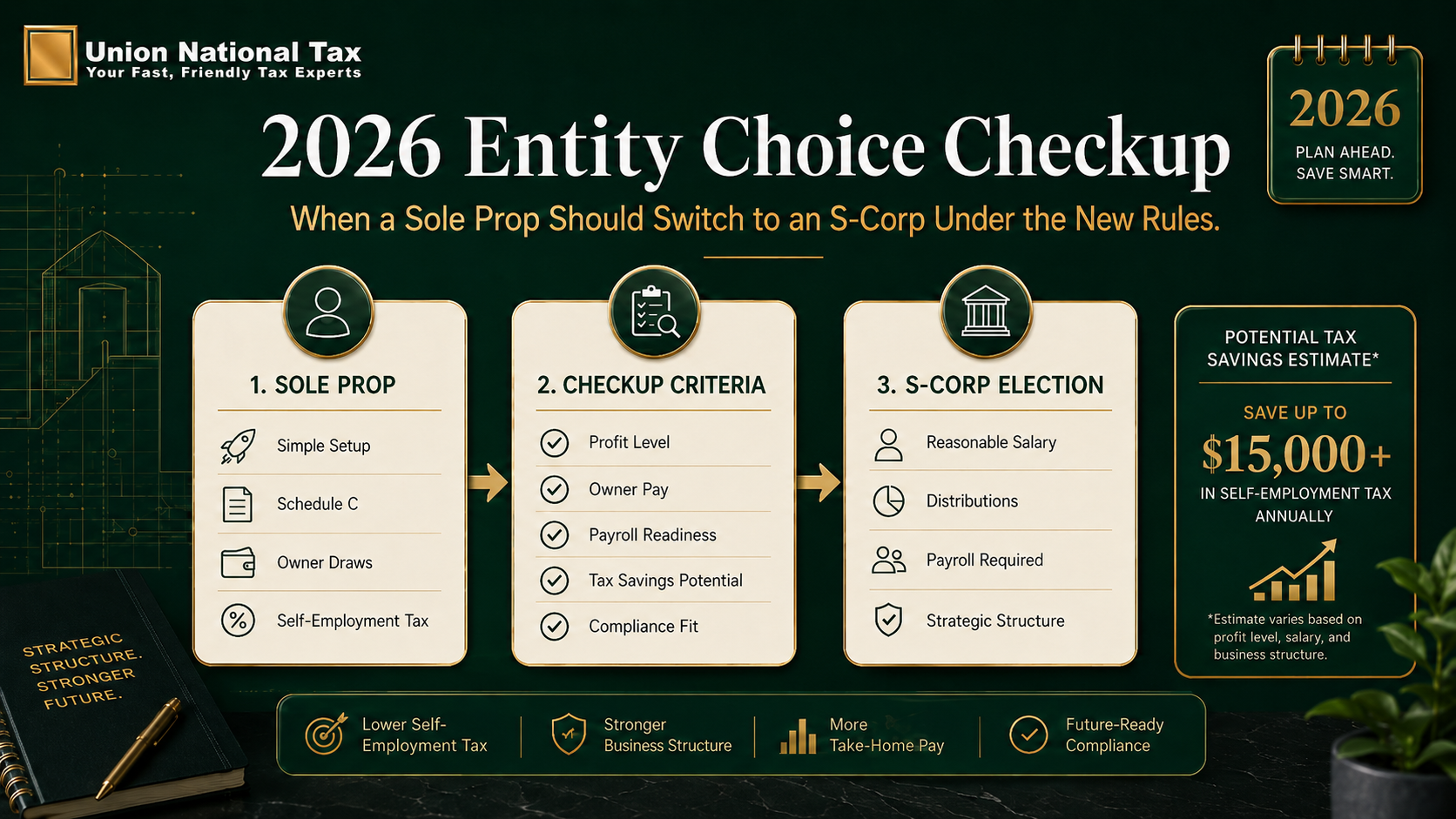

Sole prop vs. S‑corp: 2026 basics

As a sole proprietor or single‑member LLC, your net business profit is generally subject to both income tax and the full 15.3% self‑employment tax. It is simple and flexible, but as profits climb, the payroll tax bill climbs right alongside them.

An S‑corp is still a pass‑through for income tax, but you split earnings into two buckets:

- Reasonable salary (subject to payroll taxes).

- Distributions (not subject to self‑employment tax, though still subject to income tax).

That split is where most potential tax savings come from—and where the IRS looks most closely.

When an S‑corp starts to make sense

There is no single magic profit number, but many CPAs find that S‑corps usually begin to pencil out once your consistent net profit crosses a certain threshold.

Rules of thumb for 2026:

- Below roughly $60,000 in steady annual profit: the added complexity and payroll costs often outweigh any savings.

- Around $60,000–$150,000+ in profit: an S‑corp often produces meaningful self‑employment tax savings if you pay a defensible salary and take the rest as distributions.

If your profit swings wildly from year to year, it may be worth waiting until you see a stable pattern before electing S‑corp status.

How 2026 QBI rules factor in

Under the post‑OBBBA rules, the QBI deduction of up to 20% of qualified business income is now permanent and still applies to qualifying pass‑through businesses such as sole props, S‑corps, and many LLCs. That matters because both structures can qualify; the difference is how salary interacts with QBI.

In an S‑corp:

- Salary is not QBI‑eligible, so higher wages reduce the amount of income that can get the QBI deduction.

- Distributions are QBI‑eligible, so shifting some profit from wages to distributions can increase the slice that gets the 20% deduction.

In practice, you are balancing three forces:

- Reducing self‑employment tax by shifting profit from wages to distributions.

- Preserving as much QBI‑eligible profit as possible.

- Staying within the IRS’s idea of reasonable compensation for your role and industry.

That trade‑off is why running scenarios (ideally with a pro) is important before you flip the S‑corp switch.

Reasonable compensation: IRS expectations

You cannot pay yourself a token salary and call everything else a distribution without inviting scrutiny. The IRS expects S‑corp owner‑operators who work in the business to take reasonable compensation as wages for the services they perform.

Key factors in a reasonable salary analysis include:

- Your role and responsibilities (hands‑on owner‑operator vs. more passive owner).

- Industry norms and what you would pay someone else to do the same job.

- Time spent in the business and the business’s overall profitability.

If the IRS decides your salary is unreasonably low, it can reclassify distributions as wages and assess back payroll taxes, penalties, and interest.

Non‑tax trade‑offs: complexity and admin

Even when the dollar math favors an S‑corp, the structure is not free. You typically add:

- Payroll processing or software for your own wages.

- Separate S‑corp tax filings and possibly extra state filings.

- More formal bookkeeping and documentation around salary decisions and distributions.

If you are not ready for that level of discipline—or do not have support to handle it—sticking with a sole prop or standard LLC a bit longer may still be the better call, even at higher income levels.

Quick 2026 S‑corp checklist

You might be ready for a serious S‑corp conversation if:

- Your business has at least $60,000–$80,000 in consistent annual profit after expenses.

- You expect that profit level or higher to continue, not just spike for one year.

- You are willing to run legitimate payroll for yourself and keep cleaner, more formal books.

- You want to proactively manage self‑employment tax and take full advantage of 2026’s permanent QBI framework.

From there, the next move is to have a tax pro model your current sole prop scenario against a 2026 S‑corp scenario so you can see real after‑tax dollars, net of payroll costs and advisory fees.